Top 5 Considerations for Enterprise Blockchain Integration

Blockchain technology is transforming established systems and causing industry disruption with its unique capabilities. Enterprises need fresh solutions to stay competitive, while also reducing inefficiencies tied to their existing infrastructure. Blockchain introduces significant growth potential for businesses, but the technical details are still in flux, with much of the industry still in an early development phase. Before committing to a blockchain solution, here are 5 key factors to consider before getting started:

1. Difference between blockchain and cryptocurrency

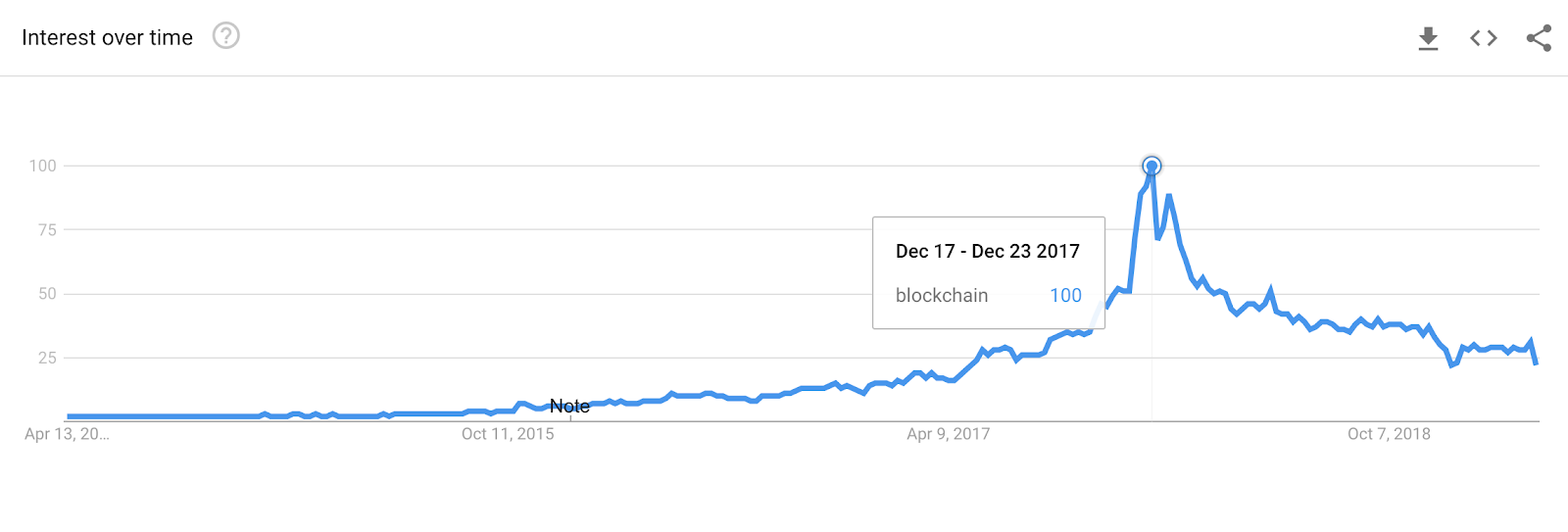

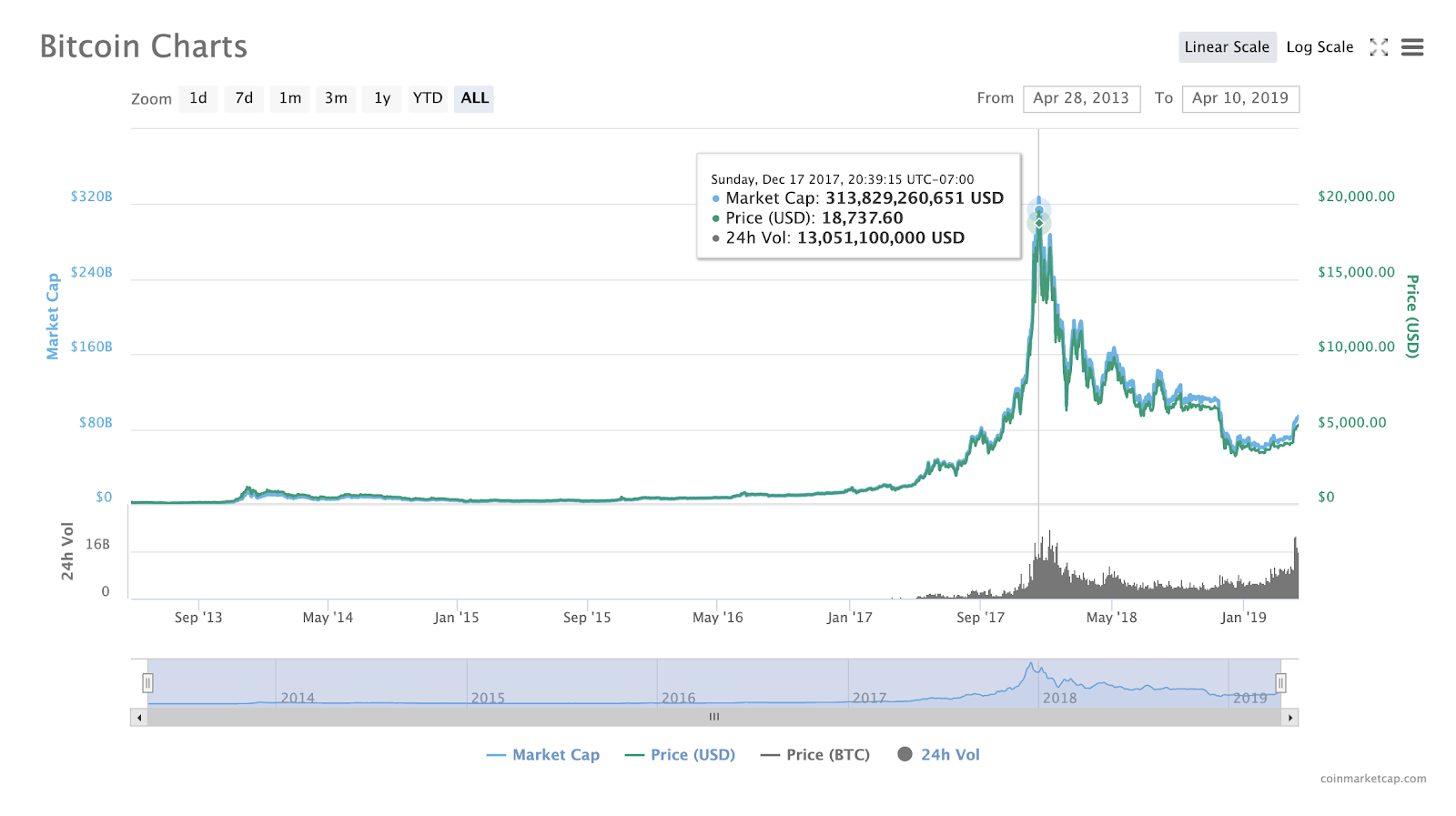

Blockchain search results vs. Bitcoin price chart

According to statistics on Google searches for blockchain, the peak of blockchain interest aligns with the peak of the cryptocurrency market. Since then, over 90% of blockchain projects have failed. The majority of consumers that entered the blockchain space became aware of the technology during the 2017 hype phase, blind to the blockchain use cases outside of cryptocurrency. Companies that managed to resist the crypto winter have focused their efforts on project-building and development, in hopes of creating a viable solution.

In order for your blockchain solution to be successful, it must be designed to withstand the volatile nature of the cryptocurrency market. A sudden shift in the price of Bitcoin should not be the determining factor behind your project’s longevity; your project needs to be able to protect itself from external threats such as price volatility.

2. Adoption

Although visual representations of blockchain have done a decent job of making the technology more approachable, most people just want to see it in action. The truth of the matter is doesn’t look pretty on the inside. Like most backend interfaces, a blockchain solution needs to be layered behind a distinguishable user interface that looks presentable to the end user. Users won’t adopt a system that is difficult to use or understand.

Along with the need for a structured user flow, security concerns also present a stumbling block for users trying to break into blockchain. According to a 2018 PwC survey on blockchain, although “84% of respondents are actively involved or searching for blockchain technologies, 45% of them believe that trust is a delay in terms of adoption." Are you managing CPNI or sensitive consumer data? When considering a solution, it's important to understand the characteristics of the blockchain, whether it’s public, private, or permissioned, and ensure that the solution abides by the GDPR regulation.

In the blockchain space, customer data is a key factor, especially given blockchain’s association with decentralization. The last thing you want your blockchain project to do is collect too much information; you should know exactly what the project needs from the end user and protect that data at all cost.

3. Does it have to be on the blockchain?

Are there alternative/more efficient solutions to blockchain integration? If so, then move on-don’t try to reinvent the wheel. The benefits of using the blockchain must be clearly defined and outweigh those of existing systems. According to Deloitte’s Global Blockchain Survey, “while more than 41 percent of respondents say they expect their organizations to bring blockchain into production within the next year, 21 percent of global respondents—and 30 percent of US respondents— say they still lack a compelling application to justify its implementation.”

Decision makers need to see how blockchain is improving their workload and how it can actually help improve internal processes. The proposed blockchain solution needs to have a proof of concept that’s meaningful, not just be another “blockchain project”.

4. Knowing your audience

Just like any other product offering, you must make sure to clearly define your intended target audience. Introducing a blockchain project in a heavily-saturated industry may not be the best idea. Also, be aware that the regulatory environment in some countries may conflict with, so be sure to work closely with a compliance agency to ensure that your project abides by local laws.

As of 4/24/2019, there are over 2100+ registered cryptocurrency projects, so you have to ask yourself some questions before diving in. Are competitors also using blockchain solve the same problems as you? How will blockchain help differentiate your business and how will it improve the experience of your staff and/or customers?

5. Limited resources

Blockchain projects require developers that understand the technology clearly and are able to create a customized solution suited to solve specific business problems. Blockchain resources are fairly scarce, so the need to source blockchain developers may be a barrier in itself, especially for a small business. Although there are Blockchain as a Service providers offering hybrid solutions, the amount of development resources available solely for blockchain may be limited. If your project will utilize existing blockchain applications like Ethereum, smart contract implementation will require you to hire someone with knowledge on Solidity, Ethereum’s smart contract language. According to Glassdoor, there are approximately 2000 blockchain-related positions available. On Dragonchain, you can run smart contracts in languages existing developers already use and know for years. This includes C++, Go, JavaScript, Java, Python, Ruby, Shell, C#, Hy, Rails, PHP and others.

Conclusion

Blockchain adoption will take time and patience. Until then, it is imperative that the community continues to educate others on blockchain and its potential. For more resources to help you determine if blockchain is right for your business, please download our free Enterprise Blockchain as a Service project planning guide.